Latest industrial R&D scoreboard shows only modest growth in investment, but promising outlook for European health and energy sectors

Photo credits: Foto-event / BigStock

The growth in research and development spending by Europe’s top firms slowed in 2024 to its lowest level since the Covid pandemic in 2020, according to the latest figures from the European Commission’s Joint Research Centre.

The annual EU Industrial R&D Investment Scoreboard analyses the activities of the world’s top 2,000 R&D investors, which account for almost 90% of global private R&D funding.

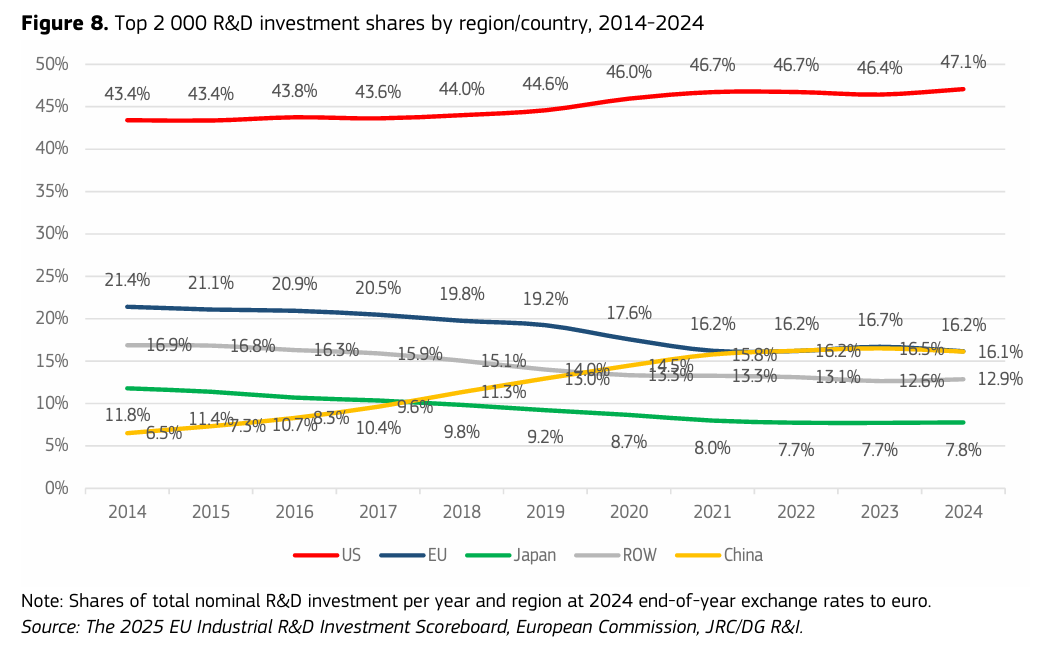

R&D investments by EU-headquartered companies grew 2.9% in 2024 to €234 billion. But this is well below the previous year’s 9.3% increase and, excluding 2020, represents the lowest rate of growth since 2014. The increase is also smaller than in the US (7.8%), Japan (7.1%) and China (5.2%). The result is that Europe’s share of investments has been progressively shrinking for a decade.

The ranking of the world’s top companies by R&D investment illustrates what economists have called Europe’s “middle technology trap.” Whereas the US economy is now characterised by high-tech software firms, Europe’s car companies remain its largest investors in R&D. Four EU-based firms make the top 30 global investors in R&D. All four are German automotive companies: Volkswagen, Mercedes-Benz, BMW and Bosch.

The EU’s automotive sector invested €87 billion in R&D in 2024, more than any other region. However, its R&D growth was sluggish at 0.8%, outpaced by Chinese and Japanese automotive companies, which increased investments by 11.9% and 12.3% respectively. This suggests European manufacturers risk being supplanted in the transition to electric and autonomous-driving technologies.

Meanwhile, the top five global R&D investors are all US information and communications technology (ICT) firms: Amazon, Alphabet, Meta, Microsoft and Apple. R&D investments are increasingly concentrated among these companies, which have doubled their share of global investments over the past decade to around 15%.

ICT software is the fastest-growing sector, from 13% of global R&D in 2015 to 25% in 2024. However, EU R&D investments in the field fell by 8.9% in 2024 as its companies exited the top 2,000 and key players reduced their investments.

Reasons for optimism

In certain sectors, notably health and energy, European growth in R&D outpaced other regions. EU companies in the health sector increased R&D investments by 13% in 2024, a higher rate of growth than both the US (7.1%) and China (0.1%). This was driven by significant investments by large pharmaceutical companies. Denmark’s Novo Nordisk increased R&D by 29.4%, while Germany’s Bayer oversaw a 22.6% increase.

This comes despite warnings from drugs companies that an upcoming reform to the EU’s pharmaceutical legislation, first proposed in 2023, would push investments outside of Europe. An agreement was finally reached in December 2025 that offers stronger incentives to drug developers than the initial proposal, but industry says it still does not go far enough.

Related articles

- EU R&D spending increases, but still falls short of 3% target

- Better together? EU car industry pins hopes on joint R&D

R&D investments in the EU’s energy sector grew by 19.8%, outpacing the US, Japan and China. The European aerospace and defence industry also registered 4.8% growth in R&D investment, reflecting an increased political focus on defence readiness and European autonomy.

Private R&D spending is an important political issue, as it’s an arena in which Europe continues to lag behind. More than two decades ago, EU countries set the target of raising public and private R&D spending to 3% of GDP but, even today, the EU average remains around 2.2%.

This is significantly below global competitors, and the gap is largely explained by a lack of private investment. In the EU, business-funded R&D accounts for around 57% of total expenditure, versus 70% in the US and 79% in China, according to Eurostat.

Receive the Funding Newswire [full access requires a subscription] each Tuesday, our Policy Bulletin each Thursday, and the fortnightly R&D Express, tracking reforms and investments in central and eastern Europe.

Receive the Funding Newswire [full access requires a subscription] each Tuesday, our Policy Bulletin each Thursday, and the fortnightly R&D Express, tracking reforms and investments in central and eastern Europe.

A unique international forum for public research organisations and companies to connect their external engagement with strategic interests around their R&D system.

A unique international forum for public research organisations and companies to connect their external engagement with strategic interests around their R&D system.